There has been a lot of yapping about Medivolve Inc. (MEDV.NE) (COPRF) on all of the stock groups and chat boards lately. So I decided to take a look. There are generally two types of penny stocks. The undervalued gems that you have to find yourself and the hyped up ones that are spoon fed to you by pumpers.

MEDV seems like a weird combination of both. The latest Q3 results

show $25 million in revenue and $7 million in net income. But the market cap

is only $53 million at $0.135. Annualizing the net income and slapping a

10 P/E on it would justify a $280 million market cap or about a $0.70

stock price. This would kind of make sense if no one heard of this

stock. I've seen Canadian juniors trade like this before. However, not

in the way that MEDV is trading.

For the two weeks since the financials were released, millions of shares have traded each day. The company is very IR friendly and going strong with the promotion right now. You can't turn your head in Canadian penny stock land without some jackass trying to stuff this stock down your throat. It's not undiscovered. There's something very strange going on. A stock is not simultaneously underhyped and overhyped. MEDV doesn't have a buying problem, which is what would normally plague an undervalued company. It has a SELLING problem. Despite millions of shares being bought, there are tons of sellers at these apparent "cheap" prices. These sellers would presumably know all about the Q3 financials and yet are selling anyways. Why?

Now I know the NPC-equivalent to penny stock traders would ape "SHORTS!!! SHORTS!!! SHORTS!!!" on this like mindless drones. I'm so sick of that stupid argument. Not every stock is manipulated and shorted, and those who do it are doing it for good reasons and are smart. They aren't interested in getting themselves into short squeeze situations. Let's just say this. Whether it's shorters or sellers, SOMEONE is very confident that MEDV is NOT significantly undervalued at a $53 million market cap despite initial apperances of a stock worth at least five times that amount. To the point where they are willing to dump/short millions of shares even as the hype train from retail shareholders is at full steam ahead.

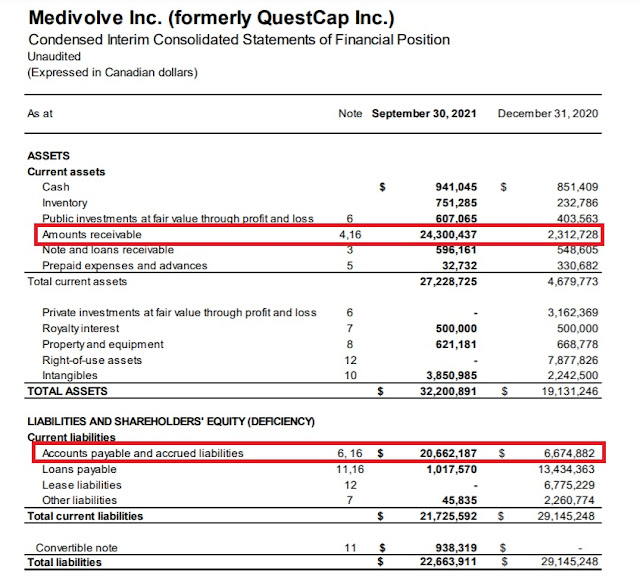

A few minutes of looking at the financials and you'll see why this is. Shown below is MEDV's Q3 balance sheet.

Despite the positive net income, there is an operating cash outflow of $8 million year-to-date. That has resulted in the company issuing $17 million worth of equity in dilutive private placements to pay off debts and keep the lights on.

This is accounting 101, a red flag you want to look out for. An exploding A/R balance is a sign that a company is not actually collecting on the revenues it's booking. It's *traditionally* a way for companies to commit fraud by overstating revenues.

Now I say traditionally because MEDV is not necessarily doing this. Maybe MEDV will get that cash in the next quarter and the A/R balance will come down. But this is something that shareholders have to keep a close eye on in future financial reports. The longer and larger that A/R balance grows, the more dubious the revenues appear to be. For now it's too soon to tell one way or another, but presents a big risk that pumpers either don't have the will or the financial knowledge to properly explain to people. MEDV isn't undervalued. The market just has some reservations about its business model.

In any of these future MEDV shareholder webinars, the absolute first question that management should address is the accounts receivable balance and receivables turnover. Because if those things are going out of control in the wrong direction, it doesn't matter how high the revenue growth or how much profitability has been generated by booking accounting revenues. The revenues need to be considered extremely low quality until collected in cash, given the circumstances.

There is one line in the financial report from a couple of weeks ago that may seem just fine and great to many new investors, but is a huge, huge no-no for me:

"Transitioned from a cash pay business model to Insurance Reimbursements increasing daily gross revenue and revenue per patient compared to the legacy cash-based business model used since the Company's inception"

This is one of the WORST and trickiest business models you can undertake as a small company. Instead of getting the cash upfront, MEDV is now performing the services, booking the revenues, then will go after insurance companies for the cash. Sure a company can increase business and pricing by going after an insurance reimbursement model. Just like your local Walmart could probably increase its revenues temporarily if it invited everyone in to grab what they could and charge their insurance for it. The challenge is NOT garnering the revenues for goods and services here. The challenge is getting insurers to pay for it. Clients are more than happy to come in and receive health care services if they think they won't be paying any out-of-pcoket expenses.

However, MEDV is this little no name company and insurance companies are some of the biggest and strongest institutions in the world. What if the insurance companies say "no, we don't think your claims are valid. We won't pay out these bills". What's its recourse? Sue them? The insurance companies have a far bigger and better legal team, and all the politicians with their SuperPAC donations will be on their side not MEDV's.

If the insurance companies deem these expenses non-reimbursable AFTER the services have been performed, MEDV will have no recourse. The expenses will have been spent to perform those services and earn those revenues, but no cash is actually coming in. The company would have to book reversals to the revenue and instead of big net income, it's big net loss numbers.

When looking at the second number I highlighted in red on the balance sheet, accounts payable, one will realize the potential financial suicide would happen swift and hard. The A/P line has exploded to over $20 million. The expenses that have occurred in order to provide the services that generated the revenue are piling up as bills. Those bills belong to creditors that will come knocking on the door hard if they think MEDV is struggling to turn its revenue IOUs into cash. They'll have to move quick like buzzards on a recently dead carcass. What happens then? Bankruptcy and the stock is worthless.

Now I'm not saying this will happen with certainty. Maybe MEDV will collect on the reimbursements sent to the insurance companies just fine. But until the company demonstrates that it can, this is a BIG risk to the investment thesis here. That's why MEDV appears so "cheap".

There are basically two extreme outcomes right now and maybe a third middle of the road one. The positive outcome will be MEDV collecting on the vast majority of revenues in cash over the next couple of quarters. Let's say 80% or more. The company proves that its business model is robust and follows up Q3 with a couple more similar quarters as well as vastly improved balance sheets and cash flow statements reflective of that successful cash collection. The stock price gradually moves up over those several months to something in the $0.50-$1.00 range, or maybe higher if more revenue growth is proven and forecasted.

The negative outcome is MEDV failing to collect on the reimbursements and has to write off a lot of its revenue. Creditors see that the company is in trouble. Perhaps the OSC investigates and the stock is halted as financials have to be restated. Bankruptcy would be a very real outcome in this situation and it would happen fast.

The third scenario is kind of a middle ground. The business isn't a complete bust, but reimbursements are hard to come by. The company has to write off revenues but not to the point where it's unprofitable and creditors pick away at the bones. The retail trader's dream of an easy 10-bagger is smashed, but they don't lose all their money either. This scenario likely results in the stock staying pretty rangebound, let's say $0.05 to $0.25.

Those are the three scenarios. I'm pretty neutral on the stock given the risks and potential rewards. What I see right now is a stock that is being heavily dumped by sellers and picked up by mostly less experienced buyers who are inept at analyzing financial statements. Some of the sellers could also be equally inexperienced and financially inept, but it's guaranteed that not all of them are. So I think the advantage is skewed to the sellers right now.

I am not buying, but I will keep an eye on this stock. If the company proves it can collect cash on audited financial statements (not future promises made on webinars that are protected by forward looking statement clauses), I will consider a long position. Even having to pay $0.25 post audited financials presumably due in March/April would leave a lot of upside if this business model is, in fact, robust. But avoiding a buy now also avoids a ton of downside risk that is clearly being ignored by the pumpers as they push this "too good to be true" easy 5 to 10 bagger scenario.

No comments :

Post a Comment